The 15-Minute Weekly Habit That Builds Financial Control

I used to dread managing my business finances.

It wasn't that I didn't understand the importance; I knew it mattered.

My problem: it felt like one more task I had to keep up with while juggling the demands of running a business—serving clients, meeting deadlines, and trying not to overlook anything important.

A lot of small business owners I have spoken with throughout Los Angeles and Orange Counties feel the same way. They know they need to stay on top of their finances, but the thought of sitting down with the numbers feels overwhelming.

The good news is that once you have a basic process in place, it does not have to take hours.

As we wrap up this April series on building a Contract-Ready Reserve or Business Stability Fund, one thing has become clear.

The biggest hurdle is not complexity. It is consistency.

In my business, I follow a simple weekly routine every Sunday morning that takes about 15 minutes. That one habit helps me see what is happening, stay ahead of expenses, and avoid the year-end scramble at tax time.

This system did not happen by accident.

I created it with my late husband, who was a retired accountant. He brought the accounting logic. I brought the small business reality.

Because the truth is, a process does not help you if it is too complicated to maintain. It has to work in real life.

For many micro and small businesses, that is the real starting point. Not a perfect financial system. Just a consistent habit of checking the numbers before they become a problem.

Why Weekly Works

For most micro and small businesses, especially those with just a few clients or projects, financial activity is manageable.

You don’t need to track everything every day.

But waiting until the end of the month, or worse, the end of the year, creates stress and leaves too much room for missed details.

Charges get miscategorized, payments don’t clear, tax deadlines sneak up, or automatic debits hit before there is enough money in checking to cover them comfortably.

A weekly review helps you catch those issues while they are still small.

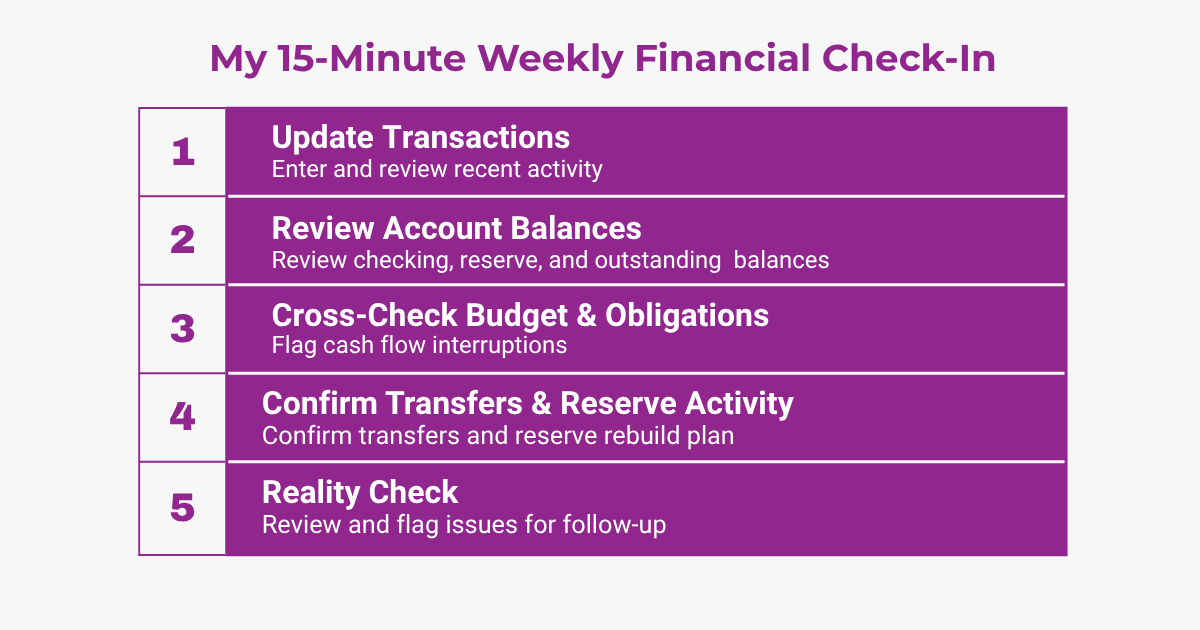

My 15-Minute Weekly Check-In

The graphic below shows the full five-step routine I use each week.

A simple 5-step weekly financial check-in can help small businesses spot problems before they interrupt cash flow.

In short, here is what I am checking:

1. Update Transactions

I manually enter my transactions using Quicken.

Other businesses may use QuickBooks, another accounting system, a spreadsheet, or a bookkeeping process set up by their accountant. The tool matters less than the habit.

For me, manual entries help me stay aware of where the money is going. The goal is not just clean records. The goal is to avoid being surprised by my own business.

2. Review Account Balances

I take a quick look at business checking, my reserve account, and outstanding balances.

I am not doing a deep analysis. I am checking whether things look stable and whether anything needs attention before the week starts.

3. Cross-Check Budget and Obligations

This is where I look for anything that could interrupt cash flow.

Upcoming payments may include tax deadlines, insurance premiums, software renewals, automatic debits, or other obligations that can fall due at the wrong time.

For a small business, one missed detail can throw off the whole week, sometimes longer.

4. Confirm Transfers and Reserve Activity

Because I am actively building a reserve, I make sure transfers are actually happening.

If the reserve is in a high-yield savings account at a different bank, transfers may take a few days to post.

I also make sure that if money is taken from the reserve, there is a plan to replenish it. Otherwise, the reserve slowly stops being a reserve.

5. Do a Quick Reality Check

At the end of the 15-minute process, I ask one simple question:

Is everything moving in the right direction?

If yes, I am done.

If not, I either make a small adjustment or add the issue to my weekly task list for follow-up.

For small business owners, if something requires more than a small adjustment, it may be time to reach out to an accountant, bookkeeper, or other qualified advisor.

Why This Matters

This routine is not just about being organized.

It is about not getting caught off guard.

I have worked with solo operators and firms generating nine-figure revenue. Their systems do not look the same, but the need for financial clarity and discipline is the same.

For the small businesses I work with, readiness is not just paperwork. It is also the ability to meet obligations, make decisions, and respond to opportunities as they arise.

If you are trying to move into government work, you need more than interest. You need stability.

You need to know whether you can handle the next opportunity before you chase it.

This is also why I keep saying that readiness is not just a subcontractor issue. The same readiness systems that help subs become compliant also help primes stay competitive and manage their teams.

In public contracting, one business’s lack of readiness can affect the timeline, paperwork, payments, and performance of everyone connected to the project.

The Real Benefit

One of the biggest benefits of this habit is what it does for tax time.

Because I update my records weekly, I am not trying to recreate an entire year from memory. My transactions are already categorized, my accounts have already been reviewed, and my records are already in good shape.

That does not make tax preparation fun. But it does make it easier.

What If You Do Not Have a System Yet?

If you are not using accounting software or a formal budget, do not let that stop you.

Start with what you have.

Log in to your bank portal once a week and review the last seven days of activity. Look at deposits, payments, pending charges, and anything that looks off.

That may not be a full system yet, but it is a start.

Whether you eventually use Quicken, QuickBooks, a spreadsheet, or another process, the first step is building the habit of looking at your numbers consistently.

And if you do not know how to set up categories, track reserves, separate business expenses, or read basic reports, consider engaging a bookkeeper, accountant, or qualified advisor to help you set up a system you can maintain.

Final Thought

Financial control does not come from doing more.

It comes from doing the right things consistently.

That is the point of a Contract-Ready Reserve or Business Stability Fund. It is not just about setting money aside. It is about creating a simple way to know what is happening before pressure builds.

Sometimes, that starts with just 15 minutes a week.

If you are a small business looking to move into government work, grab my Subcontractor Readiness Checklist to see where your business stands and what systems may need attention next.

About Stephanie:

Stephanie Clark-Ochoa is a Government Procurement Strategist and founder of Clark-Ochoa Business Services. Through Help 4 LA Subs, she provides practical tools and insights to help micro and small businesses in the Greater Los Angeles area become government-ready and thrive in public contracting.

Disclaimer: This post is for informational purposes only and does not constitute legal, financial, or professional advice. Please consult a qualified advisor before making any business-specific decisions.

🔜 Next Time on the Blog: The Lead Generation Trap: Why More Opportunities Won’t Fix a Readiness Problem